Share this

by Piera Rossi on Mar 7, 2022, 1:19:44 PM

Sometimes it may feel like our credit score dictates our lives. Everything from mortgage applications to personal loans seems to require a strong credit history. But what if you have a few damaging strikes on your report? Missed or late payment marks stay on your credit report for seven years. It seems a little unfair that seven-year-old mistakes dictate your financial life in 2026.

Moreover, some of us don't have any credit history. How are we supposed to apply for the first loan without a credit report to boast our reliability?

Fortunately, there's something called a bad credit loan. Anyone with a less than perfect credit score no longer needs to feel ostracised by lenders. A bad credit personal loan might be the ideal solution to your financial worries.

What Is a Personal Loan and What Can I Finance With It?

A personal loan is a credit product lenders offer for borrowers to spend however they choose. They're typically smaller than mortgages but might have higher interest rates. Generally speaking, personal loans are unsecured—meaning that the borrower doesn't have to offer up any of their assets as collateral.

Borrowers can spend personal loans on just about anything. With unsecured loans, once the lender has handed over the money, you can do whatever you like with it. Many choose to spend the funds on medical expenses, travel, weddings, home renovations, emergencies, or consolidate debt.

If you're considering a personal loan, remember that other options are also available. For example, you could open a credit card account. Credit cards allow you to spend a certain amount each month. If you pay back your borrowings on time, you might not even get charged interest. However, those with a poor credit history might struggle to get approved.

Personal loans might be the solution to your finances. It's the ideal way to borrow the necessary funds. Moreover, repaying it on time might even improve your credit score.

Can I Get a Personal Loan Approved if I Have Bad Credit?

Yes, the door to personal loans isn't shut just because your credit score may be a tad weak.

Your credit report is documentation of all your debt and credit usage. Your score goes up and down depending on how you manage your finances. Those with high credit scores are deemed more reliable. Those with lower scores might have unpaid debts or missed payments marking their report. A bad credit report might inhibit your chances of finance approval in the future.

While lenders look at credit scores, they also consider other criteria, such as your income, other debts, and collateral. The lender might approve your loan application despite your credit score if you can supply documentation that proves your financial security and reliability.

Additionally, many lenders offer bad credit loans.

With poor or nonexistent credit history applicants in mind, bad credit loans are less favourable to the lender than the standard personal loan. People with bad credit are a higher risk to the lender. If you have a history of missing your repayments or worse, the bank will judge that you are unreliable. Accordingly, they will charge higher interest rates or other fees to protect themselves.

The same goes for anyone who doesn't have a credit score. If you're young or have never taken out a loan, you may not have had time to build your score. Therefore, the lender cannot ascertain your risk level. Evidence of income and other financial documents will help. However, you may also need to opt for a bad credit loan.

Types of Loan for Bad Credit

Each lender has a different way of constructing a bad credit loan. Some require borrowers to put up an asset as collateral, while others offer guarantor loans. If you're unsure which option suits you best, speak to a finance broker who will be able to provide independent advice.

Let's check out some of the different types of loans for bad credit borrowers.

Secured Loans

The most common bad credit is the secured loan. While most personal loans are unsecured—no collateral is put up—some lenders offer secured loans to those with poor credit.

A secured loan is when you offer asset security against your borrowings. If you fail to repay the lender, they have a legal claim to your asset. They then use this to compensate for their losses. If you're a high-risk borrower—i.e., have a low credit score—then a secure loan protects the lender.

Car loans or mortgages are usually secured loans. The borrower puts the house or car up as security against the loan. However, you could offer other assets, such as jewellery or fine art, stocks or bonds, and other valuable items. Secured loans are one way of keeping your interest rates down if you have poor credit.

However, ensure that you're aware of the risks. If you default on your payments, you may lose your asset. Therefore, it's crucial that you only take out personal loans you know you can afford. If you have a bad credit score, ask yourself whether you are in an excellent position to take out a loan. Remember, if you miss your payments on a new loan, you will only worsen your credit score.

Guarantor Loans

Another option for bad credit borrowers is a guarantor loan. You'll need someone, usually a friend or family member, to guarantee on your behalf that you'll repay the loan.

Therefore, your guarantor is legally bound to repay the remainder of the loan and interest if the borrower defaults. Because of the added risk, guarantor loans typically have higher interest rates than other personal loan options.

The advantage of a guarantor loan is that you can use it as a chance to improve your credit score. By making repayments on time, you can build up your score. You may also borrow more than with other bad credit loans.

Ensure that both you and your guarantor understand the consequences should you not pay. Are they in a financially stable enough position to repay the loan on your behalf? The lender will check their credit history to ensure lower risk. However, as a guarantor, it can be easy to forget to factor other's loans into your budget.

In some circumstances, the lender pays the funds directly to the guarantor. They will then need to pass on the money to you.

To be a loan guarantor, you must meet the following requirements:

- Aged 18 or over

- Be an Australian citizen

- Have a good credit score

- Have stable income

Bad Credit Personal Loans

Finally, bad credit personal loans are like regular ones—unsecured and without a guarantor. However, they have much higher interest rates and perhaps other fees. If you can't offer any collateral or a guarantor, a bad credit personal loan might be your only option.

Bad credit personal loans also often limit how much you can borrow. Similarly, they may restrict the loan term. Yet, they might be pretty expensive in the long run. If you default on a repayment, you will face significant consequences. Aside from hitting your credit score, the lender might also trigger legal action to get their money back.

You may need extra documents to qualify for a bad credit personal loan. These might include payslips and utility bills.

Why Choose Bad Credit Loans?

Like with any credit product, there are pros and cons. You must assess whether bad credit loans are suitable for you as a wrong decision may have severe consequences.

The best thing about a personal loan designed for bad credit is that you have a greater probability of approval. With a secured or guarantor loan, you can offset your risk level. Even if your credit score is not too bad, these types of loans may get you better rates.

Furthermore, bad credit loans aren't restrictive. Often, we think that our options are limited when we have poor credit scores. However, as with a standard personal loan, you can tailor your bad credit loan to monthly, fortnightly, or weekly repayment plans. Personalised plans can help you keep track of your payments and ensure you don't miss one.

You can also get flexible loan terms. Most lenders will be amenable if you prefer a longer loan term with lower monthly repayments. However, it's worth remembering that longer loan terms cost more in the long run as more interest builds up. Yet, it's still an option if your budget struggles to stretch to higher monthly repayments.

Finally, taking out a loan and repaying it on time is an opportunity to repair your credit score. With each monthly repayment, you should see your score creep back up.

That said, there are a few risks to consider. A bad credit loan may come with higher interest rates, caps on the amount you can borrow, and collateral assets.

How High Are Interest Rates on Bad Credit Loans?

Generally speaking, most lenders will mark up their interest rates if you have poor credit. As you're considered a higher risk, the extra interest payments protect the lender should you default on your payments. While every lender's interest rates differ, you might expect to pay around 2 - 2.5% or more in interest. The amount you pay will largely depend on your lender and your credit rating.

Some bad credit loans have interest rates as low as 10%. Yet, you should often expect to pay more. However, with a guarantor or secured loan, you may be able to negotiate the interest rate.

What Are the Fees and Charges if I Have a Bad Credit Rating?

Interest rates aren't the sole factor in shopping around for personal loans. Many bad credit loans brag lower interest rates but charge higher fees elsewhere. For example, you may get pulled in by a 10% interest rate on a bad credit loan but have to pay a hefty loan application and service fees.

Accordingly, make sure that you look at the comparison rate. All lenders have to advertise a comparison rate on all loan types. The comparison rate shows you the loan's actual cost, combining interest rates with other charges. While a low-interest rate is beneficial, the comparison rate is more important.

What Can I Spend My Bad Credit Loan On?

We mentioned that you could use a personal loan for just about anything. Is the same true of a bad credit loan? Well, it depends. If your bad credit loan is secured, there are probably some restrictions on how you can use the money. For example, if you offset the risk of your loan against a car, the lender might stipulate that the entire loan amount must go towards the car.

On the other hand, if you get approved for an unsecured bad credit loan, you should use the money however you choose. However, the lender will usually ask anyway. If you plan to use the funds to consolidate debt, you may struggle to get approved as debt consolidation doesn't necessarily improve your financial situation.

What to Consider When Taking Out a Loan With Bad Credit

No loan is without risk. Both the lender and borrower face some level of danger. However, if you have bad credit already, the consequences might be even more significant. Therefore, you must think about what you're doing ahead of time.

Is the Loan Affordable?

Firstly, you need to think about whether your loan is affordable. The lower your credit score, the less favourable your loan terms are. You may have calculated that you can afford to repay the principal, but can you manage the interest and other fees? Generally, the lower your credit score, the less you can afford to borrow.

Take time to make sure that the repayment schedule suits your monthly budget comfortably. Moreover, consider how long the loan will last. While lower monthly repayments might seem attractive, is it sensible? Bad credit personal loans are better for short-term solutions. A loan term of seven years on higher interest rates could significantly weaken your finances. Can you negotiate a shorter loan term?

Alternatively, if you're already stuck with a bad credit loan, you may be able to refinance. After a year of regular repayments, your credit score should go up enough to get better loan terms with the same lender or elsewhere.

Deposit

While it's not always necessary, some lenders require a deposit for bad credit loans. Deposits generally are for larger loans. For example, if you want to buy a car for $30,000, can you save up to $6,000? Deposits are one way of proving to the lender that you are responsible with your money. Even a deposit of as little as 10% will showcase your ability to put aside money each month.

As with secured and guarantor loans, offering a deposit might help lower your interest rates. Speak to your lender about whether this is an option.

Defaulting Will Be Costly

Before taking out any credit product, you need to understand the risks and consequences of defaulting. If your repayment is late, you may have to pay the penalty. Any payment between 14 and 60 days is late - most lenders have a fixed fee, around $15 - $30. They will also charge extra interest on the missed amount. Finally, the late payment will get marked on your credit score.

One late payment won't make a significant difference to your credit score. However, if it becomes a common occurrence, your score will dip.

If your repayment is later than 60 days, this is a defaulted payment. As a result, if you cannot repay the debt, the lender will claim your collateral or request the repayments from your guarantor. But if you have neither, you may have to face legal action.

Limits to What You Can Borrow

Manage your expectations as to what you can borrow. As lenders deem you a high risk, they're less likely to let borrowers with low credit scores apply for large sums of money. Each lender has different limits. However, you'll probably find it hard to get approved for any loan amount above $50,000.

Remember, this isn't just in the lender's best interest. If you have a poor credit score, taking on a huge debt is a significant risk. The more considerable the loan amount, the more you pay in interest and the longer the loan term. Therefore, there is a greater chance of a missed payment or default. As we mentioned earlier, only take out a loan you can afford.

Tips to Get a Bad Credit Personal Loan Approved

So, how do you get your bad credit loan application approved? With an already delicate credit score, you don't want to risk damaging it further with rejected applications.

- Maintain transparency throughout the personal loan application. If you know you have a poor credit report, don't try to hide it. The lender will find out sooner or later. Any mistruths or discrepancies in your application will only work against you.

- Try to ensure your finances look healthy. For example, don't drain your bank account on payday or apply for many credit cards within a short period.

- Consider improving your credit score before applying. There are several ways you can do this, which we'll cover further on.

How Do I Know My Credit Score?

If you have ever applied for credit before, you'll have a credit score. You can access your credit report for free once every three months. It's a good idea to check it at least once a year, especially if you're thinking of applying for a new loan.

Your report consists of your rating (the magic number that indicates "low", "fair", "good", etc.) and the details of your credit history. For example, it will have black marks for previously missed payments. You can access your report online, by email, or by mail from the three leading credit reporting agencies. These are Experian, Illion, and Equifax. Each agency might score your credit differently.

At Ausloans, we help you make informed decisions with our Borrowing Power Calculator. Do you want to know how much you can borrow? Well, to calculate your borrowing capacity (how much you can borrow) we first need to collect a little information about you and your credit history. We need this information to run a soft credit check to get your credit score. Don't worry it only takes a few minutes and this won't affect your credit rating.

How Do I Know I Need a Bad Credit Loan?

Surprisingly, not everyone who thinks they have bad credit needs a bad credit loan. You may qualify for a regular loan. Start by taking a look at your credit report. If you have any black marks or a low score, then speak to a lender or broker about whether you'll need a specialist loan.

Finance brokers are in the best place to help you find the best loan to suit your situation. If your credit isn't as bad as you think, don't get sucked into paying higher interest rates than you need. Similarly, a broker will help you avoid applying for loans that won't approve you.

What Happens if Previous Loan Applications Were Rejected?

The lender conducts a soft inquiry into your credit report when applying for a loan. This shouldn't impact your score at all. However, after offering pre-approval, the lender will make a hard inquiry. This signifies taking on new debt, causing your score to dip slightly. If you're approved, then it won't have any long-term effects.m,

However, if the lender rejects you after the hard inquiry, this may prevent you from getting approved elsewhere. It is especially the case if you receive several loan application denials in a short period.

Can You Build Your Credit Score With a Personal Loan?

A bad credit score doesn't have to stay bad for long. If you take on a personal loan and repay the money on time, then it won't be long before your score starts to build up again. Bad credit personal loans are one way of getting out of the bad credit slump. Just make sure that you don't miss a payment and further damage.

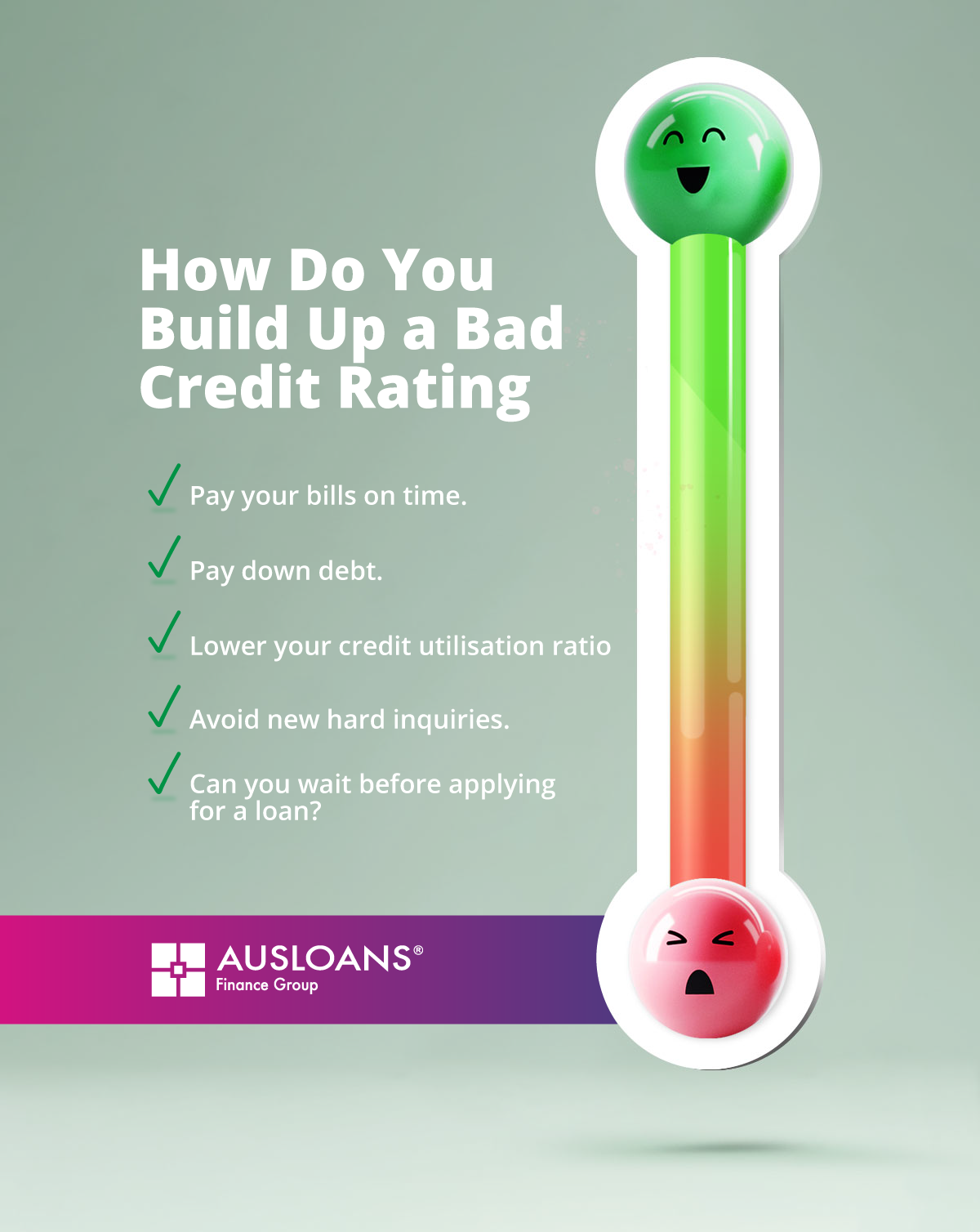

How Do You Build Up a Bad Credit Rating?

Unfortunately, it seems easier for your score to go down than up. That said, here are several ways to improve your credit score.

- Pay your bills on time. Regular repayments of debt and other bills will ensure that your credit score stays level. Your payment history makes up more than a third of your score. An excellent way to ensure you never miss a payment is to set up automatic transfers.

- Pay down debt. If you have several maxed-out credit cards, try to pay off as much as you can. Experts recommend that you not use more than 30% of your credit limit beyond the monthly repayment date.

- Lower your credit utilisation ratio. If you have two credit cards with a limit of $5,000 each, spread your debt between them.

- Avoid new hard inquiries. Don't apply for loans or open credit accounts that lead to hard inquiries.

- Can you wait before applying for a loan? Negative marks drop off your report after seven years. If you’re not in urgent need of the funds, it might help to wait for your score to improve.

How to Apply for a Bad Credit Loan?

Firstly, research your loan options. Speak to a broker about which bad credit personal loan is right for you. Once you have found a suitable product, apply online. Personal loan applications are straightforward. Secondly, you'll need to supply supporting documentation, such as ID and evidence of income.

Your chosen lender will respond with a personalised rate and pre-approval. The next step is to sign on the dotted line and begin budgeting your repayment schedule.

Is a Bad Credit Personal Loan Right for Me?

Taking out a loan is not a light decision. As we've seen, the consequences for defaulting on your loan repayments can be severe. However, if you can afford the payment plan, a bad credit loan could suit your situation.

If you need a quick lump sum to finance a medical bill or treat yourself to a holiday, applying for a bad credit personal loan might also help you turn your credit score around.

Whatever your reason for your lower credit score, a personal loan tailored to your circumstances might solve all your financial problems.

Can I Refinance a Bad Credit Loan?

As they come with higher interest rates, bad credit loans are not ideal long term solutions. However, if all you can afford is a longer loan term than you'd like, don't worry; you won't be stuck with it forever. After a year or so of repaying your loan on time, you should have built back your credit score enough to refinance your loan with the same lender or go elsewhere.

Refinancing a bad credit loan should get you access to better interest rates, lower fees, and a shorter loan term. Speak to a broker about what loan terms you can expect when you refinance.

Bottom Line

Bad credit personal loans are a flexible option for those who struggle to get finance from mainstream banks. Credit scores aren't the be-all and end-all of loan approval. Remember to use other documentation to prove your financial reliability. Moreover, consider getting a guarantor or applying for a secured loan.

Bad credit loans might have higher interest rates and less favourable terms. However, they are an excellent option if you cannot find approval for regular loans elsewhere. And, with regular repayments of your new loan, your credit score will soon bounce back.